I'm seeing red

What a Gas

Winter is coming. Time to make sure that the larders are full, and that the supply lines are open and ready should they be needed. Too bad for us that one of the most crucial supplies, that of gas, comes not from our own side but from, well, from beyond the Wall, so to say. From the Others.

So, if the mood sours between us and the Others, we had better have good supply alternatives, or sufficiently filled stores. Or both. Given that the mood has been gradually becoming more hostile for quite some time now, by now we surely have alternative suppliers lined up, internal networks up and running, and a good amount of gas squirreled away in our own storage facilities? In particular for those regions abutting the Wall, who’d be the first to feel the chill?

Alas, far from it. Our internal supply networks are still precarious and inefficient, alternative suppliers not yet secured and pipelines nearly non-existent, and storage… well, storage could be a good deal better.

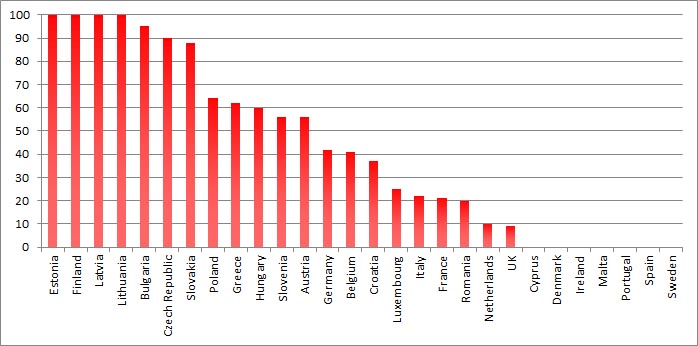

Europe has wasted precious years in reducing its dependence on Russian gas. As the table below shows, a good portion of the Eastern EU members import more than 50% of their gas from Russia, the Baltics and Finland even 100%. Germany, with more than 30%, is also quite vulnerable.

Dependency on Russian Gas Imports (share in consumption, 2012)

Source: CIEP

An interactive chart from DICE shows how this dependence has evolved over the years. While some improvement is discernible, the situation is far from reassuring. And some decisions simply defy understanding, such as the cancellation of the Nabucco pipeline, which would have offered an alternative that does not originate in nor goes through Russia; the selfish German decision to go for the Nordstream pipeline, which seemed to provide energy security to the country but at the price of increasing its dependency on one supplier while bypassing Poland, a staunch German ally; and the decision to sell Germany’s (and Europe’s) largest gas storage facility to Gazprom, the state-controlled Russian gas monopolist.

Hopefully, the new geopolitical reality will help to concentrate minds. Hopefully, too, we will have enough time to improve energy security. After all, winter is coming.