The size of the parliament-approved rescue packages for Greece, Ireland and Portugal raises hackles across the Eurozone. But it has surfaced that an even larger bailout has been tolerated by the European System of Central Banks (ESCB) for the past three years that dwarfs the officially approved ones.

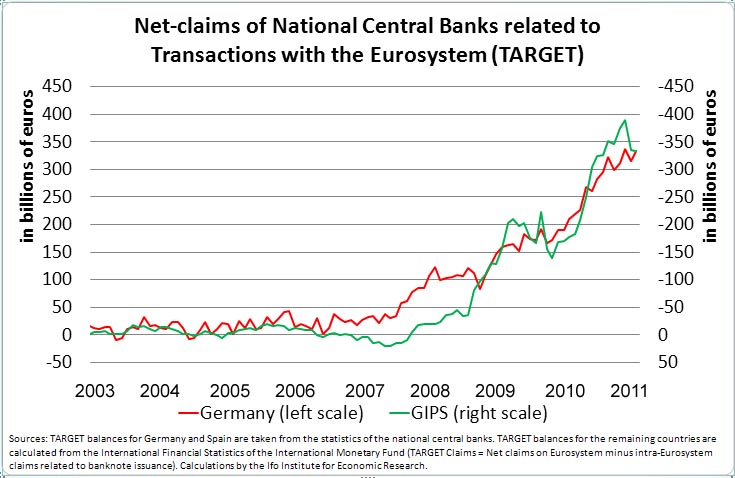

The key to measure this bailout is Target, the eurozone’s central bank clearing house for the settlement of interbank payments. The Target balances show that, as the financial crisis hit and private credit dried up for the stricken economies in the eurozone’s south and western periphery, the central banks of Greece, Ireland and Portugal and, to some extent, also of Spain (let us group them under the term GIPS), started to finance the current account deficits instead. They did this by lending out more money than was needed for internal circulation in their respective countries, enough at any rate to pay for goods and assets bought from other euro countries, notably Germany. Often this extra lending was done against low-quality collateral. In effect, the whole operation amounted to a forced transfer of capital from the central banks of the stable European countries to those of the stricken economies in the periphery. Huge asset and liability positions have accumulated now among the central banks, with the GIPS the biggest debtors and the Budensbank the biggest creditor. We are talking about 344 billion euros in GIPS liabilities and 326 billion in Bundesbank claims.

As Hans-Werner Sinn—who first brought the issue to public attention with articles in such German papers as Wirtschaftswoche, Süddeutsche Zeitung and Frankfurter Allgemeine Zeitung a few months ago—now points out, this must stop: in two years it will no longer be possible to offset the extra money printing and central bank credit extension in the GIPS countries with a corersponding reduction in the other euro countries. Unless, of course, the European Central Bank relinquishes its mandate to safeguard the currency’s stability and allow the euro to slide into an inflationary phase. The situation is serious.

The entire issue is a bit more complicated than the simple outline above. For more details, read a VoxEU article by Hans-Werner Sinn on the issue, and the excellent article on the Financial Times by Martin Wolf (the latter only for registered users).

|