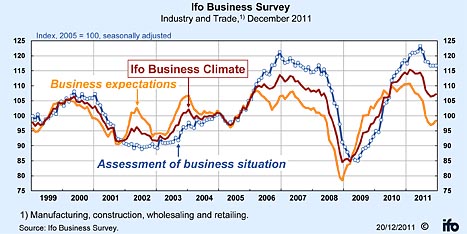

The Ifo Business Climate for trade and industry continued to improve in December after stabilising in the previous month. Survey participants continued to assess their current business situation as favourable, while their expectations for the coming six months improved for the second time in succession. The German economy seems to be successfully countering the downturn in western Europe.

The business climate brightened in construction, wholesaling and retailing, and remained unchanged in manufacturing. Business expectations in all four survey sectors are more optimistic than in November. With the exception of manufacturing, evaluations of the business situation are more positive than last month. In manufacturing the situation is no longer assessed quite as favourably as last month, but the business situation nevertheless remains good on the whole. Overall, the results show that the German economy remains very stable in a challenging international context. There is no decline in activity to be seen at the moment.

The Ifo Employment Barometer fell slightly in December, but companies are continuing to recruit additional staff. Employment growth, however, is expected to continue at a slower pace. In manufacturing the employment barometer fell for the third time in succession. Staff numbers are deemed too high somewhat more frequently, and reports of staff doing overtime were less frequent. Gentle growth in employment is nevertheless expected to continue, with mechanical engineering companies particularly seeing a need for additional staff. Car manufacturers, on the other hand, have significantly downsized their staffing plans. Willingness to recruit has also declined in retailing and wholesaling. Staff planning nevertheless remains positive in these sectors. Construction companies report somewhat more frequently that they are seeking to hire staff.

The business climate in manufacturing remains unchanged. While manufacturing firms assess their current business situation as slightly less positive than in November, they still regard their six-month business outlook more positively than in November. They also see greater opportunities in the export business. Pressure due to high inventories increased slightly and companies are less satisfied with their backlog than in November.

The business climate index also rose in the intermediate goods sector. Furthermore, developments here are following a different pattern compared to the overall average. The business situation is now assessed more positively, but business expectations remain as sceptical as last month. Satisfaction with backlog levels decreased again slightly, while pressure due to high inventories rose.

Meanwhile, capital goods manufacturers assess the business situation less positively than they did last month. Their business expectations, however, are slightly more optimistic. Firms remain more or less as happy with their backlog as they have been to date. In the consumer goods sector, in contrast, the business climate index fell, with firms now clearly less satisfied with their current business situation. They continue to see the outlook as cautiously as they did in November, and their order intake declined further.

In construction the business climate brightened. Survey participants reported a slightly more favourable business situation than in November. In terms of their six-month business outlook they are also more optimistic than previously. Unlike in December 2011, there were few complaints of weather-related constraints. Equipment utilisation is currently significantly higher than it was during the same period one year ago.

In civil engineering, however, the business climate cooled slightly, with firms assessing their current situation as poorer. Their business expectations, however, are somewhat more optimistic than in the previous month. Plans to decrease prices were less frequently reported. The business climate index rose in structural engineering. It increased in public-sector structural engineering, residential construction and in commercial construction, which saw the biggest rise this month. Companies in all three structural engineering segments assess their current business situation and their business outlook more optimistically.

The business climate in wholesaling improved again. The wholesalers surveyed are more satisfied with their business situation and more optimistic about their short-term business prospects. There was a significantly higher increase in sales versus the same period last year than in the previous month. Pressure due to high inventories has decreased slightly and there are more frequent reports of planned price increases.

The business climate brightened in business-to-business trade and wholesale consumer goods. The business situation and outlook also improved in the consumer goods sector. However, pressure due to high inventories increased again – especially in consumer goods. Price increases are planned with the same frequency as last month. In the B2B sector the business situation is more favourable than in November. Survey participants reported somewhat lower business expectations, and inventories were more frequently seen as excessive. Traders, however, reported plans to raise prices.

In contrast, the business climate in the automotive parts wholesale sector cooled considerably. The current business situation is less positive than in November. Automotive parts wholesalers were more pessimistic about their outlook while pressure due to high inventories increased significantly.

The business climate index also increased in the retailing sector. Retailers are clearly more satisfied with their business situation and more optimistic about their short-term outlook. They are planning price increases less frequently than previously. Although pressure due to high inventories increased again slightly, retailers would like to be able to restock more freely.

Moreover, developments in the consumables and durables sectors differed. In durables the business climate improved, with the business situation significantly more positive than in November and survey participants’ expectations more optimistic. In the consumables sector, however, the business climate index fell. Both the business situation and the business outlook were assessed somewhat more bleakly. Pressure due to high inventories increased again. Traders here only wish to restock a little less cautiously. In vehicle retailing the business climate index rose, with the current business situation recovering from last month’s sharp decline. Survey participants’ expectations are also no longer as sceptical as previously.

In the service sector the business climate index rose. The service providers surveyed are more satisfied with their current business situation than last month and assess their short-term business prospects more favourably. Demand for services increased at a livelier pace again and firms are increasingly looking to recruit additional staff.

Meanwhile, the business climate in the transport and logistics sector brightened slightly. Companies expect demand to develop more favourably in the near future, but they report less frequently a wish to recruit additional staff. The business climate also improved significantly in the real-estate sector, and its current business outlook is more positive than previously.

The business climate in the legal, taxation and consulting and auditing sectors improved dramatically, driven by much stronger demand. The business climate index also increased sharply in the advertising sector, where the business situation is once again significantly better than last month. However, survey participants revised downward their business expectations somewhat.

In the personnel recruitment and outplacement sectors (which include temporary employment agencies), on the other hand, the business climate brightened. The business situation is now more frequently assessed as good and firms no longer see their prospects as unfavourably as they did previously.

|